PARIS — March 2026

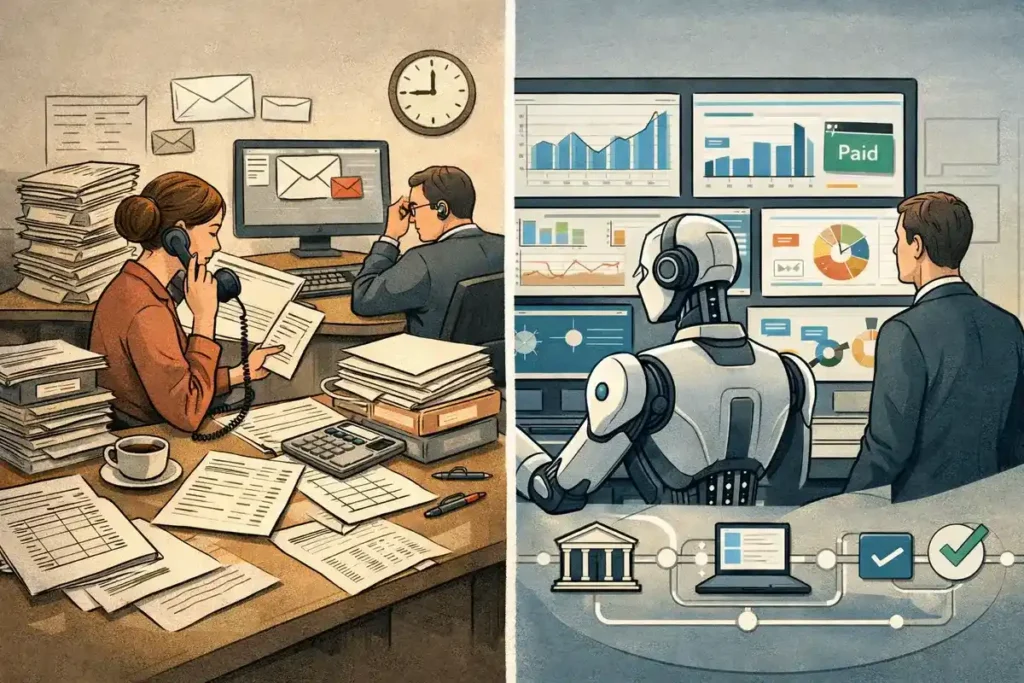

A new layer is quietly forming inside enterprise finance — one that shifts accounts receivable from a manual workflow into an autonomous system.

French startup Cleavr, founded in 2025, is positioning itself at the center of that transition. The company has raised approximately €1 million in early-stage funding to build what it describes as the first “AI collaborator” dedicated to cash collection — a system designed not to assist finance teams, but to replace large parts of their operational workload.

The premise is straightforward, but structurally significant: accounts receivable is no longer a process — it is becoming an execution layer.

From Reminder Tools to Autonomous Financial Systems

For decades, accounts receivable has been governed by a fragmented stack:

- reminder emails

- spreadsheet tracking

- outsourced collection agencies

- manual dispute resolution

Even modern SaaS tools have largely digitized — not redefined — this workflow.

Cleavr’s model departs from that paradigm entirely.

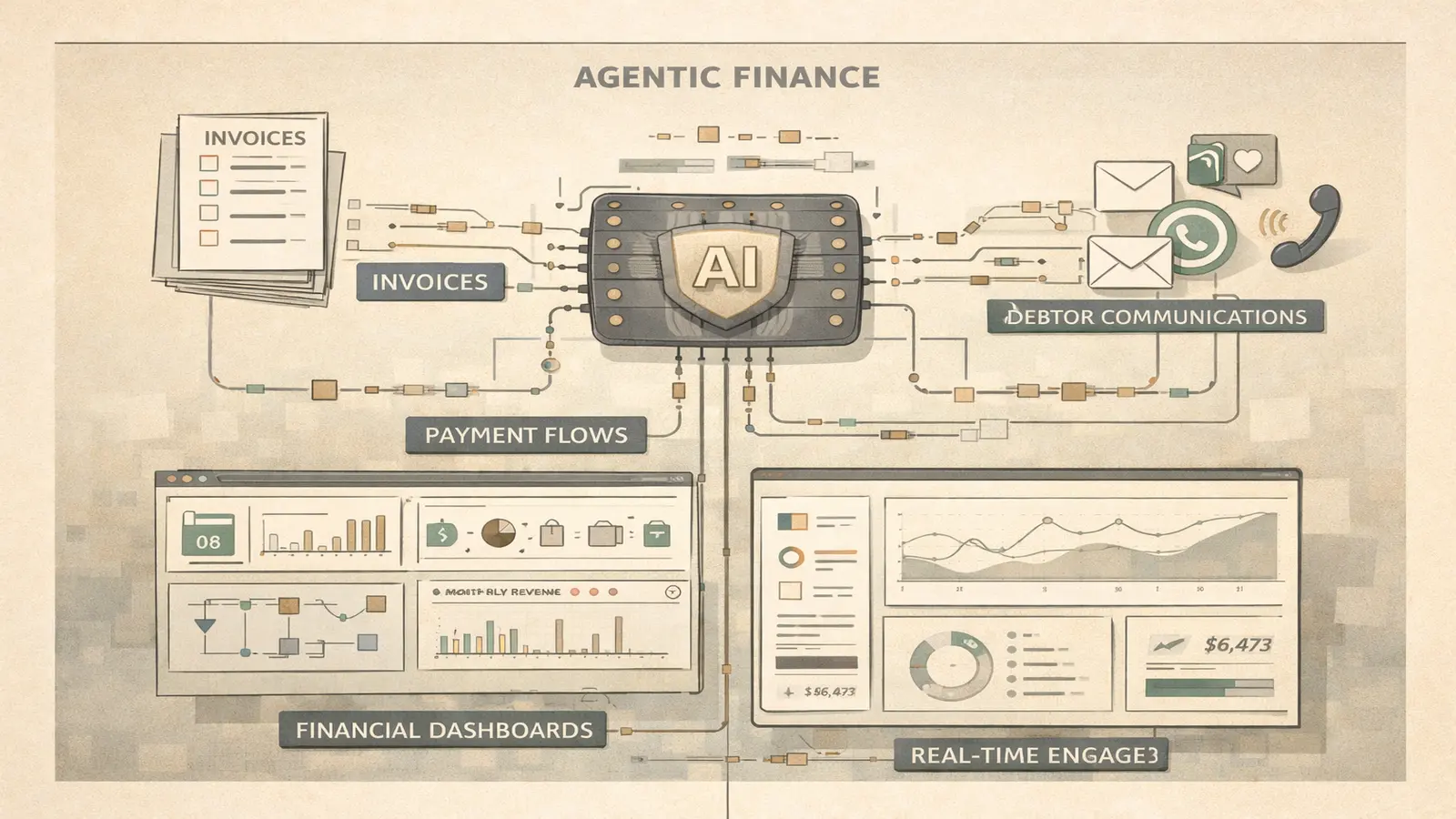

Instead of sending reminders, its system operates as an autonomous agent embedded within financial infrastructure, capable of:

- initiating conversations with debtors

- interpreting responses

- negotiating payment terms

- resolving disputes

- triggering legal escalation when required

The shift is subtle but important.

The unit of work is no longer a reminder. It is a decision.

This transition mirrors a broader shift across enterprise software — from interfaces to execution systems — as explored in our analysis of the shift from chat interfaces to AI agent systems.

Architecture: The Emergence of an “Agentic Finance” Stack

At a technical level, Cleavr reflects a broader pattern across enterprise AI — the transition from tools to systems, a shift we previously outlined in our breakdown of why the next AI breakthrough is expertise, not models.

While the company does not disclose its underlying models, observed behavior suggests a multi-layered architecture:

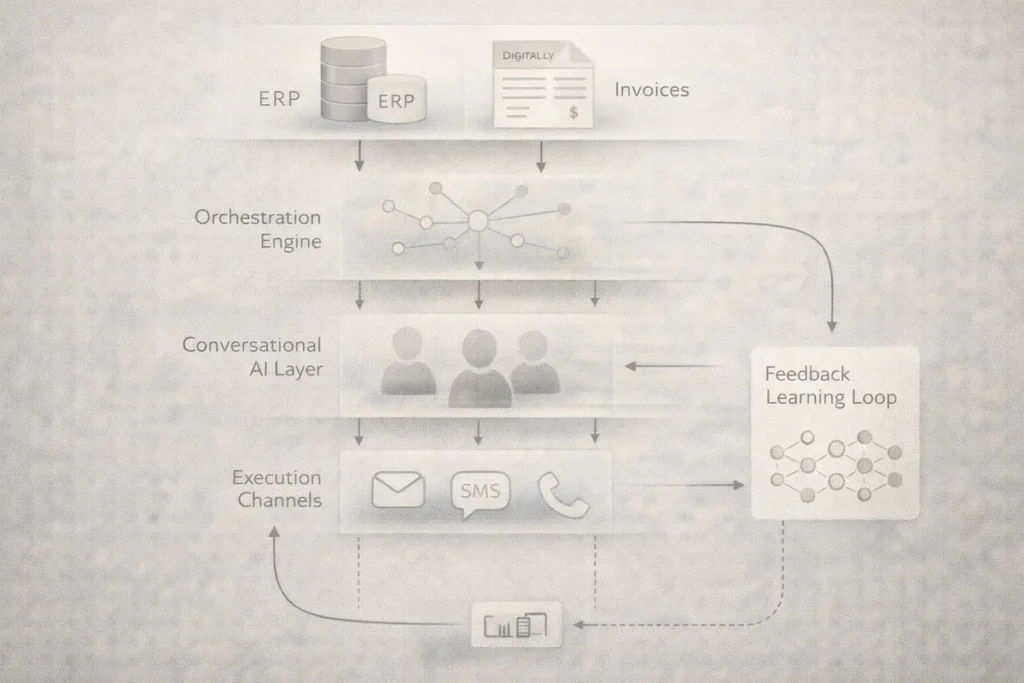

1. Data Ingestion Layer

Direct integrations with ERP and accounting systems — including Pennylane, NetSuite, SAP, and Odoo — allow the platform to ingest invoices, payment history, and customer metadata in real time.

2. Profiling & Orchestration Engine

Each debtor is modeled as a dynamic profile, incorporating behavioral patterns such as:

- payment delays

- response preferences

- communication effectiveness

This enables the system to determine not just what to say, but when and how to say it.

3. Conversational Intelligence Layer

At the core is a large language model–driven agent that:

- parses debtor responses

- assigns confidence scores (e.g., 94% likelihood of payment)

- adapts tone and negotiation strategy

Unlike traditional automation, this layer operates contextually rather than rule-based.

4. Action & Execution Layer

The system executes across multiple channels:

- SMS

- AI-generated voice calls

It also handles reconciliation, payment tracking, and escalation — including integration with legal networks across Europe.

5. Learning Loop

Each interaction feeds back into the system, creating a compounding effect:

the more it operates, the more precise it becomes.

Why Now: A Structural Breakdown in Payment Systems

Cleavr’s timing is not accidental.

France, like much of Europe, is experiencing a persistent late-payment crisis, as highlighted in European payment behavior research:

- 94% of companies report monthly cash flow loss from unpaid invoices

- average payment delays exceed 49 days

- business failures have surged beyond pre-pandemic levels

The underlying issue is structural.

Modern companies operate in real time — but their financial control systems do not.

Accounts receivable has become one of the slowest-moving layers in otherwise real-time businesses.

Cleavr’s model attempts to resolve that mismatch by turning receivables into a continuously executing system — a pattern increasingly visible across AI infrastructure layers, as discussed in our analysis of the AI startup market power shift.

Product-Market Fit: Early but Signal-Rich

Despite being less than a year old, Cleavr reports early traction:

- ~50 active clients

- deployment within 24 hours

- measurable improvements in cash flow

Early users include:

- Pennylane (finance platform)

- Greenly (climate SaaS)

Reported outcomes suggest:

- up to 40% improvement in cash flow

- significant reduction in days sales outstanding (DSO)

- near-total automation of follow-up processes

While these figures remain company-reported, they indicate a strong initial alignment between product and market need, as noted in Tech Funding News coverage of Cleavr.

Competitive Landscape: Where Cleavr Fits

The accounts receivable software market is already crowded, but segmented.

Traditional Tools

Platforms such as Chaser or basic AR systems focus on:

- reminders

- scheduling

- visibility

AI-Augmented Platforms

Companies like Gaviti and CollectAI introduce:

- predictive analytics

- workflow automation

Enterprise Systems

Players such as HighRadius operate at scale with:

- hundreds of AI agents

- deep ERP integrations

- end-to-end order-to-cash automation

Cleavr’s differentiation lies elsewhere.

It focuses on debtor-facing intelligence — not internal optimization.

In practical terms:

- others optimize workflows

- Cleavr attempts to replace them

A New Category: AI as Financial Counterparty

What Cleavr is building can be understood as a new category:

AI as counterparty

Instead of tools assisting humans, the system directly interacts with external stakeholders — in this case, debtors — on behalf of the company.

This reflects a broader transformation across enterprise AI — from tools to control layers — similar to patterns explored in our coverage of emerging AI infrastructure systems.

Finance, historically resistant to automation due to regulatory complexity, is now beginning to follow the same trajectory.

Risks: Where the Model May Break

The ambition of the model introduces several constraints.

Regulatory Risk

Debt collection is highly regulated across Europe. Tone, frequency, and communication methods are subject to strict rules.

Model Reliability

LLM-based systems introduce risks around:

- misclassification

- inappropriate responses

- lack of explainability

Cleavr mitigates this through confidence scoring and escalation logic, but the system remains partially opaque.

Cost Structure

High-frequency interactions may result in significant inference costs, particularly at scale.

Competition

Larger incumbents are already integrating generative AI into their platforms, potentially compressing Cleavr’s differentiation window.

The Strategic Implication: Finance Becomes Software Infrastructure

The deeper implication is not about collections.

It is about control.

If Cleavr’s model proves viable, accounts receivable will no longer exist as a standalone function.

It will become:

- embedded

- continuous

- automated

- invisible

In that world, finance teams do not manage collections.

Systems do.

The Bottom Line

Cleavr’s €1 million round is modest in size, but structurally significant.

It reflects a broader shift:

from financial workflows → to financial infrastructure

The company is early, and execution risks remain substantial.

But the direction is clear.

As enterprise systems become increasingly autonomous, the boundary between software and operations continues to collapse.

Accounts receivable — long considered a back-office function — may be one of the first financial layers to disappear into the system itself.

Live Update Signal

This article will be updated as Cleavr expands across Europe, releases technical details, or raises additional funding.

Research Context

This analysis synthesizes reporting from Planet Fintech, Tech Funding News, Cleavr official materials, and European payment data (Coface, OpinionWay), combined with system-level interpretation of emerging AI infrastructure patterns.