Subheadline:

From Nscale’s $2B hyperscaler push to AMI’s $1B world-model bet, capital is reorganizing around compute control and real-world AI deployment.

The Week Capital Repriced the AI Stack

Nscale, a London-based AI infrastructure hyperscaler building GPU data centers, raised $2 billion at a $14.6 billion valuation, while Advanced Machine Intelligence (AMI), a Paris-based startup developing world models for physical AI, secured a $1.03 billion seed round — signaling a shift toward infrastructure ownership and real-world AI deployment.

AI funding between March 7–14, 2026 did not produce OpenAI-scale mega rounds. Instead, it revealed something more structural: capital is concentrating on control layers as model differentiation compresses.

This shift builds on patterns already visible in recent AI capital waves reshaping infrastructure, agents, and robotics, where investment began moving beyond model development into system-level control.

Alongside Nscale and AMI, companies including Nexthop AI, Mind Robotics, and Rhoda AI each raised between $450 million and $500 million — reinforcing a pattern that is less about scale alone and more about where in the system value is being captured.

The Deals, Stripped to Their Core Signals

The largest rounds cluster tightly around infrastructure, networking, and robotics:

- Nscale — $2B Series C @ $14.6B (AI hyperscaler, GPU cloud + data centers)

- Advanced Machine Intelligence (AMI) — $1.03B Seed (world models / physical AI)

- Nexthop AI — $500M Series B (AI networking, open-source switches)

- Mind Robotics — $500M Series A (industrial robotics + foundation models)

- Rhoda AI — $450M Series A (video-trained robotics systems)

- Replit — $400M Series D @ $9B (agentic software creation platform)

- Eridu — $200M Series A (AI data center networking)

- Axiom Math AI — $200M Series A @ $1.6B (code verification systems)

The pattern is consistent: capital is rotating away from general-purpose intelligence toward infrastructure ownership and real-world execution systems.

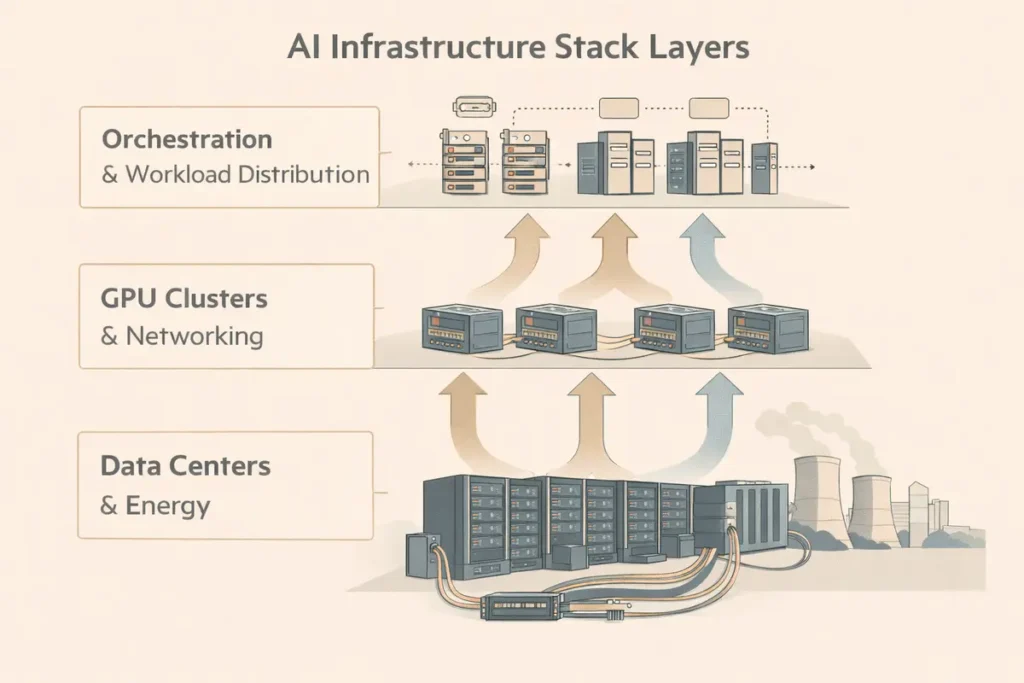

Infrastructure Is Becoming the Economic Core of AI

Nscale’s $2 billion round is not simply a scale milestone — it is a structural bet on compute sovereignty.

The company competes with European players like Rescale and DataCrunch, while positioning itself against US hyperscalers such as CoreWeave and Lambda. Its differentiation lies in vertical integration: owning data centers rather than renting compute capacity.

This aligns with broader infrastructure consolidation trends explored in Nscale’s earlier funding move, where control over compute supply began emerging as a strategic moat.

This reflects a deeper shift in AI economics. GPU access is no longer the primary constraint — control over energy, supply chains, and deployment efficiency is.

Nexthop AI and Eridu extend this shift into networking. By targeting the data center fabric — historically controlled by Cisco, Arista, and Broadcom — they are redefining how AI clusters are built and scaled.

Nexthop’s open-source network operating system introduces a different competitive model: faster iteration cycles and customer-aligned development instead of proprietary lock-in.

The result is a structural fragmentation of the AI stack into distinct layers:

- Compute ownership

- Network orchestration

- Workload distribution

Each is now large enough to support venture-scale outcomes.

Physical Intelligence Is Emerging as the Second Front

At the same time, capital is moving into what may become the next defining category: physical intelligence.

AMI’s $1.03 billion seed round positions it directly against World Labs and other robotics-focused AI companies pursuing world models — systems designed to understand physics, space, and real-world interaction.

This shift echoes the broader movement toward real-world AI explored in the rise of humanoid and industrial robotics systems, where deployment, not just intelligence, is becoming the defining constraint.

This is not an extension of large language models, but a divergence from them.

Mind Robotics and Rhoda AI extend this thesis into execution:

- Mind leverages real-world data from Rivian’s vehicle ecosystem

- Rhoda trains on large-scale video datasets to model complex environments

The competitive axis is shifting toward:

- Data origin (vehicle, video, sensor fusion)

- Deployment context (industrial vs general-purpose environments)

- Model architecture (physical reasoning vs language-first systems)

The underlying question is no longer how to generate intelligence — but how to operationalize it in the physical world.

Capital Is Following Defensibility, Not Narrative

What connects infrastructure and physical AI is not narrative — it is defensibility.

Capital is increasingly flowing toward layers where:

- Assets are difficult to replicate (data centers, proprietary datasets)

- Revenue scales with usage rather than experimentation

- Customer relationships are embedded in operational workflows

This reflects a pattern also visible in the rise of AI control plane infrastructure, where orchestration layers are becoming critical points of value capture.

The investor alignment reinforces this:

- Lightspeed and Andreessen Horowitz backing Nexthop

- Accel supporting robotics platforms like Mind

- Menlo Ventures leading verification infrastructure (Axiom)

The shift reflects a deeper recalibration:

the model layer is becoming a distribution layer, while infrastructure and deployment capture durable economic value.

The Constraint the Market Is Underpricing

AI is entering a phase where capital intensity is rising faster than capability gains.

Despite the scale of funding, both battlegrounds share a constraint that remains underpriced: execution speed.

Infrastructure companies depend on GPU supply chains dominated by NVIDIA and AMD. Any disruption — whether pricing, allocation, or geopolitics — directly affects margins and expansion timelines.

Physical AI companies face a different bottleneck: time-to-deployment. Systems operating in real-world environments require slower iteration cycles, integration testing, and reliability thresholds that software AI does not face.

This mirrors broader concerns raised in recent analysis of AI valuation structures, where capital deployment is accelerating faster than underlying system maturity.

This creates a structural asymmetry:

- Infrastructure is capital-intensive but operationally scalable

- Robotics is strategically valuable but time-constrained

The winners will be those that can convert capital into deployed systems faster than competitors — not simply raise more of it.

Competition Is Becoming Multi-Layered

Competition across these companies is not direct — it is stack-dependent.

Nscale is not just competing with GPU providers; it is competing with hyperscalers, energy markets, and financing structures. Nexthop is not simply a networking company; it is redefining how compute clusters are architected.

Similarly, AMI, Mind Robotics, and Rhoda AI are not substitutes. They are parallel attempts to solve the same systemic constraint from different entry points.

This creates a competitive environment defined less by feature comparison and more by strategic positioning within the AI stack.

Strategic Implications for Founders and Investors

For founders, the signal is clear:

the highest-leverage opportunities are shifting away from model creation toward control layers and deployment systems.

For investors, this week signals a reallocation toward:

- Infrastructure ownership

- System orchestration layers

- Real-world deployment platforms

For incumbents, particularly in networking and robotics, the threat is structural. Startups are not just improving products — they are redefining system architecture and value capture points.

AI Is Moving From Capability to Control

The most important signal from this week is not the size of the rounds, but their direction.

AI is transitioning from a capability-driven market to a control-driven system, where value accrues to those who own infrastructure, manage distribution, and deploy intelligence in real-world environments.

This is a repricing of intelligence itself.

Not as a standalone capability, but as a function of where it sits in the stack — and who controls that position over time.

Research Context:

This analysis synthesizes publicly reported funding rounds, investor participation, competitor positioning, and structural trends across AI infrastructure, networking, and robotics markets as of March 2026.

Editorial Note:

This article reflects independent analysis of publicly available information and broader AI ecosystem trends.