A pre-IPO capital push reveals a deeper shift: in emerging AI markets, system ownership—not model innovation—is becoming the primary driver of scale.

Amity, a Southeast Asia–based enterprise AI infrastructure company operating at the execution layer, has raised $100 million in Series D funding — signaling a structural shift in how AI systems are being built, scaled, and monetized outside model-centric ecosystems. The round, led by EDBI, is positioned not as exploratory growth capital, but as pre-IPO positioning — designed to consolidate assets, strengthen revenue predictability, and construct a public-market-ready operating profile.

At first glance, the raise appears to follow a familiar late-stage pattern. In structural terms, however, it reflects something more consequential: a divergence from the dominant AI playbook. Rather than competing in the increasingly capital-intensive race to build better models, Amity is building leverage through ownership of systems — acquiring legacy software, embedding AI into operational workflows, and transforming existing revenue streams into AI-native infrastructure.

This mirrors a broader shift already visible across AI infrastructure, where value is increasingly captured not by intelligence alone but by control layers that shape how that intelligence is applied (see: Why AI observability is becoming a control layer).

The result is a fundamentally different scaling model. In this framework, AI is not the product. It is the upgrade layer applied to systems that already generate value.

The Structural Shift: From Model Innovation to System Control

Much of the global AI narrative remains anchored in model development — larger architectures, improved benchmarks, and incremental gains in reasoning capability. This model-centric view assumes that intelligence itself is the primary source of value.

Amity operates on a different assumption: that the majority of economic value in AI will not be captured at the model layer, but at the system layer where that intelligence is applied. Enterprises do not fundamentally require more advanced interfaces; they require existing workflows to be restructured into systems that can execute decisions, automate processes, and directly impact revenue.

This reframing aligns with a growing pattern across AI startups, where execution systems — rather than copilots — are becoming the dominant architecture (see: How execution-layer AI is replacing workflows).

Instead of optimizing for intelligence, companies optimize for integration depth, workflow ownership, and distribution — the layers where long-term enterprise value historically accumulates. In this context, the strategic question is not who builds the best model, but who controls the systems through which that model operates.

Capital Logic: Engineering a Public-Market Narrative

The structure of Amity’s Series D reflects this shift in emphasis. Framed explicitly as a pre-IPO round, the capital is not intended to fund experimentation, but to engineer scale — accelerating acquisitions, strengthening the balance sheet, expanding R&D capabilities in Singapore, and building global go-to-market infrastructure.

This aligns with a broader transition in AI capital markets, where infrastructure narratives are increasingly favored over application-layer growth stories (see: Why AI infrastructure is splitting into new layers).

With annualized revenue surpassing $100 million following a rapid GenAI-driven expansion, Amity represents a relatively rare profile in Southeast Asia — combining growth with emerging signals of profitability and structural scalability. In effect, it is transitioning from a venture-backed growth story into a public-market infrastructure narrative.

The underlying logic closely resembles private equity roll-ups, where value is created through consolidation and operational improvement. The distinction is that AI acts as the transformation layer.

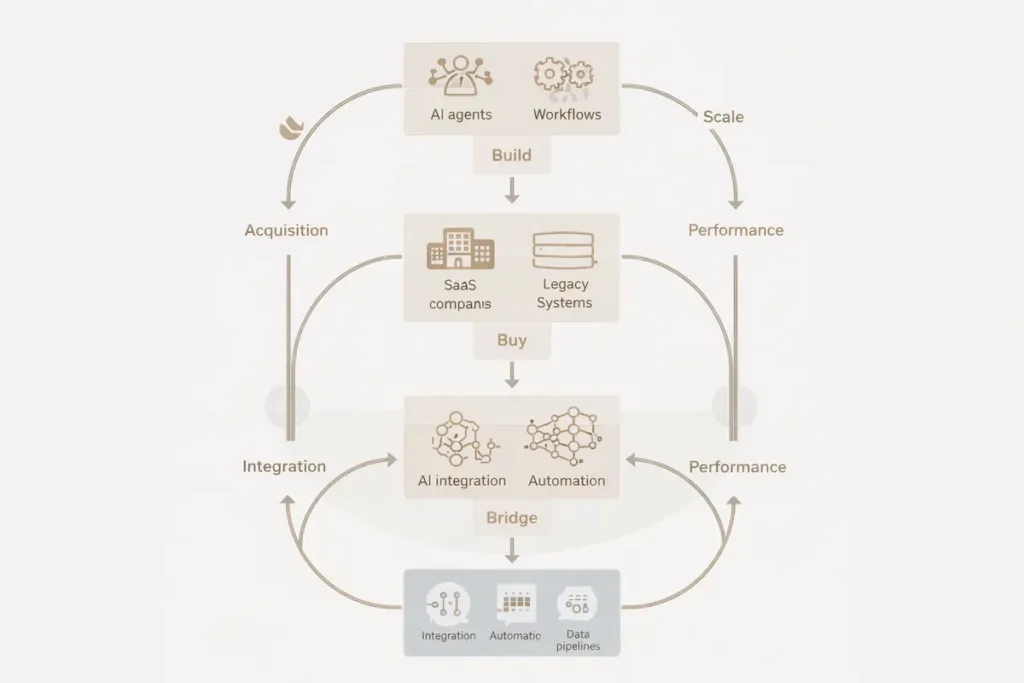

The “Build, Buy, Bridge” Engine

Amity’s model is structured around a three-layer system that defines its scaling mechanism.

The first layer, Build, focuses on developing vertical and agentic AI systems designed to execute workflows rather than merely assist them — reflecting the broader industry shift toward autonomous systems.

The second layer, Buy, involves acquiring under-optimized enterprise software assets, particularly in communications and SaaS categories. These acquisitions provide immediate access to revenue, customer bases, and operational infrastructure, effectively bypassing the constraints of organic market creation.

The third layer, Bridge, is the critical differentiator. Through this layer, Amity integrates its AI capabilities — conversational interfaces, voice analytics, and workflow automation — into acquired systems, transforming static software into AI-native platforms.

This approach mirrors how newer AI-native infrastructure companies are rebuilding legacy systems rather than replacing them outright (see: How AI-native cloud infrastructure is being rebuilt).

Together, these layers form a compounding loop: acquisitions generate revenue, AI integration improves performance, and improved performance justifies further acquisitions.

Sequencing Advantage: Revenue Before Intelligence

The core advantage of this model lies in sequencing. Most AI startups begin with technology and attempt to build distribution around it. Amity reverses that sequence by starting with distribution and layering intelligence on top.

By inheriting customers through acquisitions, the company bypasses long enterprise sales cycles and generates revenue from the outset. AI then functions as a multiplier, improving retention, increasing monetization, and accelerating growth within an existing base.

This inversion is increasingly visible across AI companies that prioritize system leverage over model innovation — a shift that is redefining how startups scale in infrastructure-heavy markets.

Geographic Architecture: Growth Meets Stability

Amity’s geographic structure reinforces its positioning. Southeast Asia serves as the primary growth engine, while Europe functions as the earnings base, with acquired businesses contributing the majority of EBITDA.

This dual structure creates a balance that is particularly attractive in a pre-IPO context — combining high-growth exposure with revenue stability and improving capital efficiency.

Competitive Position: Operating Outside the Model Race

Amity’s positioning allows it to operate largely outside the most crowded segments of the AI market. It does not compete directly with foundation model developers or consumer AI platforms.

Instead, it competes indirectly with enterprise software incumbents and infrastructure platforms — where the real battle is not intelligence, but system ownership.

However, this insulation is not absolute. Large incumbents such as Microsoft, Salesforce, and ServiceNow are embedding AI directly into their ecosystems, potentially compressing the opportunity space over time.

Constraint Layer: Integration as the Limiting Factor

The primary risk in Amity’s model lies in execution. Integrating multiple acquired systems into a unified AI-native architecture is significantly more complex than deploying standalone AI features.

If integration fails, the compounding loop breaks — reducing growth efficiency and weakening the underlying investment thesis.

At the same time, incumbents with existing distribution may not need to acquire assets, instead embedding AI directly into their platforms.

The Structural Implication: The Rise of the Execution Layer

Amity’s trajectory reflects a broader structural split across AI:

- model layer → intelligence, capital-intensive, competitive

- execution layer → workflows, integration, revenue ownership

Historically, the execution layer has captured more durable value because it sits closest to revenue generation.

Amity is positioning itself squarely within that layer.

The IPO Path: Constructing Scale

The company’s planned 2027 IPO is being actively constructed through a sequence of restructuring, expansion, and acquisition-driven scaling.

A large European acquisition in progress could significantly strengthen its financial profile before listing — enhancing revenue visibility and reinforcing its infrastructure narrative.

Long-Term View: AI Roll-Ups as a New Category

Amity represents an emerging category: AI-enabled enterprise roll-ups.

These companies do not compete by building better models. They compete by controlling systems, owning workflows, and transforming legacy infrastructure into AI-native platforms.

In fragmented markets like Southeast Asia, this approach may prove more scalable — and more durable — than model-first strategies.

Conclusion

Amity’s $100 million raise is not simply a funding milestone. It reflects a deeper shift in how AI value is being created.

The next phase of AI will not be defined solely by intelligence, but by control — specifically, control over the systems where that intelligence is applied.

And increasingly, that control is being built not from scratch, but by rewriting what already exists.

Research Context

Based on reporting from Bloomberg, Business Times, and Amity disclosures, combined with broader analysis of enterprise AI, SaaS roll-ups, and Southeast Asia technology markets.

Editorial Note

This article reflects independent analysis of publicly available information and broader AI infrastructure trends.