The frenzy is cooling. The signal is getting stronger.

Global startup funding during the week of March 23–27, 2026, remained active but notably more selective, as venture capital shifted away from February’s unprecedented mega-round surge toward disciplined capital allocation concentrated in AI, cybersecurity, healthtech, and enterprise infrastructure. While deal activity has not disappeared, the nature of capital deployment has fundamentally changed, favoring companies with clear execution pathways, measurable outcomes, and infrastructure-level positioning rather than broad early-stage experimentation.

This is not a slowdown in innovation. It is a recalibration of capital behavior.

The Weekly Snapshot: ~$500M+ in Key Global Deals

Across March 23–25, the latest consolidated funding data reveals a pattern that is less about volume and more about precision, where capital is selectively deployed into companies operating at execution-critical layers of the technology stack.

March 25

- Granola → $125M Series C

- Normal → $50M Series B

- Notch → $30M Series A

March 24

- Doss → $55M Series B

- Shepherd → $42M Series B

- Spade → $40M Series B

March 23

- Dash0 → $110M Series B

- Gimlet Labs → $80M Series A

Total (highlighted deals): ~$532M

What emerges is a clear structural signal rather than a simple weekly summary:

- mid-to-late stage rounds dominate capital allocation

- enterprise and AI-adjacent companies lead investment flow

- capital is concentrated into fewer, higher-confidence bets

The Bigger Context: A Sharp Drop from February’s Peak

To understand March, it must be framed against February, which represented one of the most capital-intensive periods in the history of venture funding, driven largely by frontier AI investments — a surge analyzed in The $189B AI Funding Surge — What It Signals About Capital Concentration.

- February 2026: ~ $189B global VC (AI-driven surge)

- March 2026 (to date): ~ $13B tracked global funding

This is not a cyclical dip. It is a structural normalization following extreme capital concentration.

February was defined by outsized, market-defining rounds:

- OpenAI → $110B

- Anthropic → $30B

- Waymo → large-scale capital deployment

March, in contrast, reflects a reversion to disciplined capital deployment:

- absence of mega-round distortion

- increased selectivity in deal-making

- emphasis on execution over narrative

AI Still Owns the Capital — But the Type of AI Is Changing

Despite the overall contraction in funding volume, AI continues to dominate venture allocation, but the internal composition of that capital has shifted significantly toward applied and infrastructure-driven systems.

Weekly AI Snapshot

- ~$300M+ AI-focused funding (early + mid-stage)

- 73%+ of Series A capital allocated to AI companies

- near-total dominance of AI within tracked seed-stage deals

However, the defining change is not quantity. It is direction.

Capital is moving toward:

- clinical and regulated AI systems (e.g., health AI)

- cybersecurity and agentic AI architectures

- enterprise observability, orchestration, and control layers

Capital is moving away from:

- pure foundation model bets without differentiation

- speculative consumer AI products

- non-ROI-driven experimentation

This marks a structural transition from:

AI capability → AI utility

Deal Structure: Fewer Deals, Larger Checks

The internal composition of funding rounds further reinforces this shift, revealing a market that is compressing around conviction rather than expanding across experimentation.

- Series A average: ~ $35M–$50M

- Seed average: ~ $7–8M

- Late-stage rounds: $80M–$125M+

At the same time:

- seed-stage activity remains resilient but selective

- mid-stage funding is increasingly constrained

- late-stage companies capture disproportionate capital

This creates a barbell-shaped market structure:

- early-stage experimentation continues

- proven companies scale aggressively

- the middle layer becomes structurally compressed

India vs Global: Divergence in Capital Structure

While global markets are concentrating capital into AI infrastructure and enterprise systems, the Indian startup ecosystem reflects a different stage of development, characterized by smaller deal sizes and more distributed capital allocation.

India Snapshot (March 23)

- Bidso → ~$7.5M

- LetzRyd → $4M

- Finfinity → $2.4M

- Workroom Automation → ~$0.74M

Weekly Context

- ~21 startups raised ~$300–360M

- significantly lower average deal sizes compared to global markets

Structural Divergence

Global markets:

- AI-dominant

- infrastructure-focused

- capital concentrated in large rounds

India:

- applied technology focus

- mobility, fintech, and automation

- smaller, distributed funding patterns

India is operating as an execution-layer market, while global capital continues to cluster around infrastructure-layer control, a divergence consistent with the broader capital narrative outlined in AI Funding Is Splitting Into Infrastructure and Physical Intelligence Bets.

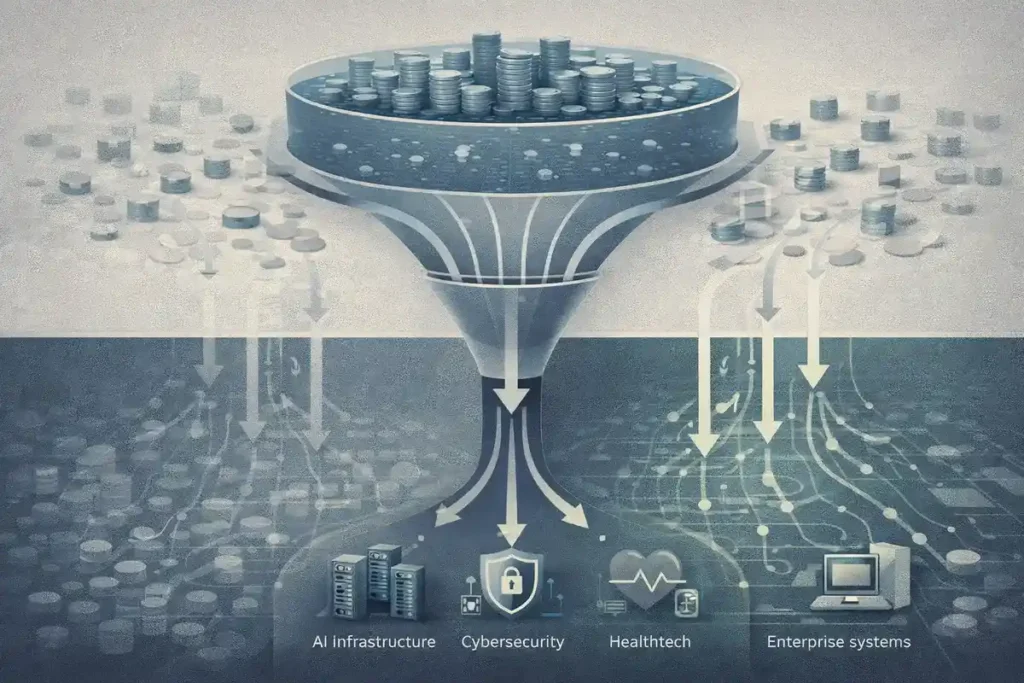

Where Investors Are Actually Betting

The most important signal is not the number of deals, but the directional consistency in where capital is flowing, which reveals a clear preference for systems that directly influence operational and financial outcomes.

Capital is concentrating in:

- Regulated industries

- healthcare

- cybersecurity

- financial systems

- Agentic AI systems

- autonomous workflows

- decision-making architectures

- execution-layer platforms

- Enterprise infrastructure

- observability systems

- orchestration layers

- data and control platforms

These categories share a defining characteristic:

They directly impact outcomes, not just outputs.

The Macro Layer: Trillions Are Coming — But Selectively

Despite short-term signals of funding compression, the long-term trajectory of capital deployment into AI and infrastructure remains expansive, driven by both private investment and hyperscaler spending.

- ~$2.5T projected global AI spending (2026, Gartner)

- $500–650B hyperscaler capex (Amazon, Google, Microsoft, Meta)

- AI expected to capture ~50% of total VC allocation

This creates a structural paradox:

- total capital availability is increasing

- access to that capital is becoming more restrictive

The Real Shift: From Hype to ROI

The most important transformation in 2026 is not the amount of capital entering the market, but how that capital is being deployed and evaluated.

Investors are no longer asking whether a company is building AI.

They are asking whether that AI:

- produces measurable outcomes

- integrates into real-world systems

- generates economic value

This shift is visible across:

- clinical outcomes in healthcare AI

- breach prevention in cybersecurity

- revenue impact in enterprise systems

The market is moving from:

exploration → execution

The Structural Pattern Emerging

Across all signals, a consistent investment architecture is forming:

1. Capital Concentration

A small number of companies capture a disproportionate share of funding.

2. Late-Stage Dominance

Value accrues to companies with proven execution.

3. Early-Stage Resilience

Seed remains active, but increasingly selective.

4. AI as Default Layer

AI is no longer a category. It is the baseline infrastructure of investment, reinforcing broader infrastructure dominance patterns explored in The AI Infrastructure Split — Who Controls the Next Layer of AI.

Why This Week Matters

On the surface, this week appears quieter compared to February’s capital surge, but structurally it provides a clearer signal of how markets behave without distortion from mega-rounds.

It reveals:

- what survives without hype

- where capital flows under constraint

- how investors prioritize under discipline

And the conclusion is unambiguous:

Capital is moving toward systems that work.

Editorial Close

The venture market is not cooling. It is evolving into a more disciplined, execution-driven environment where capital flows are increasingly tied to measurable outcomes and infrastructure-level impact.

February demonstrated how much capital exists within the system.

March is revealing where that capital actually goes.

And increasingly, it is flowing toward:

- AI systems that execute

- infrastructure that scales

- companies that deliver outcomes

Because in this phase of the market:

Intelligence is no longer enough. Execution is what gets funded.

Research Context

Based on aggregated data from Crunchbase trackers, Qubit Capital reports, startup funding databases, and market analysis as of March 27, 2026.

Editorial Note

This article reflects independent analysis of funding patterns, capital allocation shifts, and structural trends across global venture markets.