Legal AI may have just crossed into infrastructure territory.

It is no longer experimental software used by innovation teams. It is moving toward becoming operational infrastructure inside major law firms.

And Harvey’s reported $11 billion valuation is the clearest signal yet.

According to recent reporting, Harvey is raising approximately $200 million at an $11B valuation. The company has reportedly reached:

- ~$190M in annual recurring revenue

- 1,000+ enterprise customers

- 100,000+ lawyers using the platform

- Adoption across more than half of the AmLaw 100

What matters is not the size of the round but the shift it represents. Investors are increasingly valuing vertical AI companies like Harvey using infrastructure logic, where workflow embed, retention depth, and institutional dependency carry more weight than raw seat expansion.

Those are not early-stage numbers.

Those are category-defining metrics. The round, reported in February 2026, positions Harvey among the fastest-scaling vertical AI infrastructure companies.

But the valuation story becomes more interesting when you zoom out.

The Math Behind the $11B Bet

At an ~$11B enterprise valuation and roughly ~$190M in annual recurring revenue, Harvey is trading at close to 58× ARR. Similar premium infrastructure-style pricing logic has appeared in other AI verticals, including voice platforms. For searchers tracking Harvey funding, the key signal is not the round size but the speed at which enterprise usage is translating into infrastructure-style pricing.

That multiple is not pricing a SaaS tool. It is pricing infrastructure.

But in today’s environment, late-stage capital is increasingly scrutinizing durability over narrative expansion.

Some additional math sharpens the picture.

If the average enterprise client is paying roughly $16,000 per month, that implies close to $190,000 annually per customer. At current revenue levels, Harvey may be serving on the order of 1,000 enterprise clients globally.

This is not casual adoption. It suggests deep integration into mid-sized and large legal firms.

But here is where the tension begins.

Top-tier global law firms generate between $2–7 billion per year in revenue, often commanding enterprise values in the $10–20B range. Harvey’s valuation is now approaching the economic scale of the very institutions it sells to.

That raises a structural question:

Is the software layer beginning to rival the service layer in value capture?

Will Law Firms Allow AI to Replace Billable Work?

Legal economics are built on billable hours, partner leverage, and associate pyramids.

If Harvey reduces the time required to complete legal work, firms initially benefit through improved margins. However, over time, clients may demand lower fees as efficiency increases.

Law firms will embrace tools that enhance throughput and reduce risk.

They will be far more cautious about tools that compress revenue.

This distinction matters.

If Harvey increases total capacity and improves compliance while preserving pricing power, it becomes a margin enhancer.

If it merely reduces hours without expanding value, resistance will quietly build.

The valuation assumes the former.

Is an LLM Wrapper Defensible?

The most persistent criticism of vertical AI companies is structural:

Are they durable platforms, or temporary abstraction layers on top of foundation models?

If Harvey were simply an interface layered over OpenAI or Anthropic, its risk profile would be significantly higher. Base model providers could eventually ship competing legal copilots with deeper integration.

What protects Harvey is not model access.

It is workflow entrenchment.

True defensibility would require:

- Deep integration into law firm document systems

- Proprietary fine-tuning based on legal feedback loops

- Enterprise-grade security, compliance, and liability frameworks

- Relationship capital across major firms

If those layers deepen, switching costs rise.

If they do not, 58× ARR becomes fragile.

The Real Risk Is Not Competition. It’s Value Capture.

The deeper structural risk is not another startup.

It is vertical integration.

Large firms could build internal AI capabilities.

Microsoft could embed legal workflows into Copilot.

OpenAI could launch domain-specific enterprise layers directly.

The question is not whether AI will transform legal work.

It is who captures the economic upside.

If Harvey becomes the operating system of legal workflow, the valuation looks prescient.

If law firms internalize the AI layer, or if base model providers commoditize it, the multiple compresses quickly.

What $11B Is Actually Pricing

The valuation is pricing:

- Enterprise entrenchment

- Durable retention

- Infrastructure-level stickiness

- Expansion beyond research into core legal operations

It is not pricing novelty.

It is pricing control.

And that is why this is not simply an AI funding story.

It is a test of whether vertical AI companies can own value in industries long dominated by human capital.

To understand whether $11B is justified, we need to examine both the acceleration and the structural economics behind it.

The Valuation Acceleration

The funding timeline helps explain why investors increasingly view Harvey as infrastructure rather than application software.

Harvey’s climb has been unusually fast — even by AI standards.

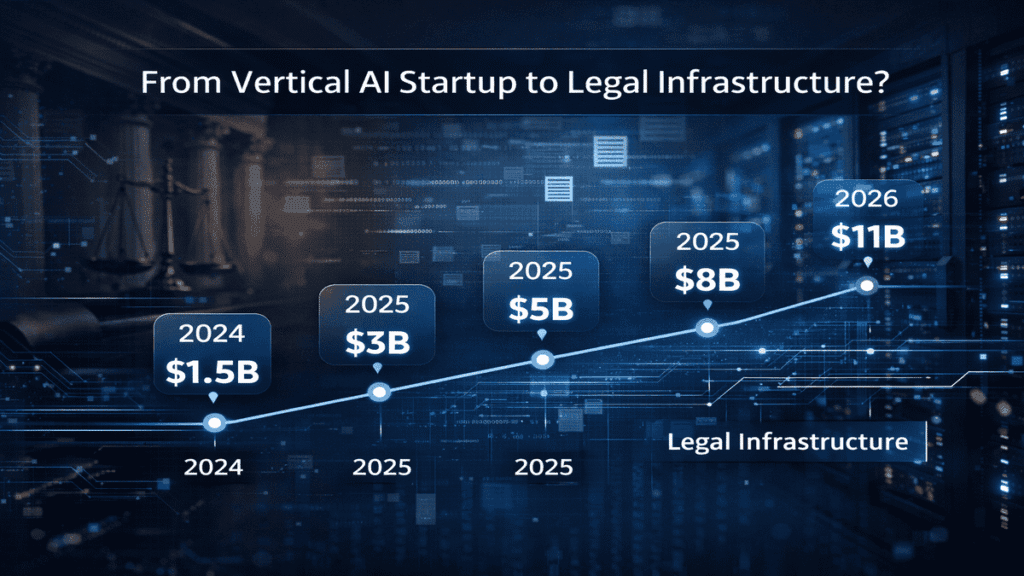

In mid-2024, the company was reportedly valued at around $1.5 billion after raising $100M in a Series C round.

By early 2025, it raised again at approximately $3 billion valuation.

Just months later, another round pushed valuation to around $5 billion.

Later in 2025, a reported raise valued the company at $8 billion.

Now, it is being priced at $11 billion.

That trajectory — from $1.5B to $11B in under two years — reflects more than hype.

It reflects investor belief that Legal AI is becoming foundational.

Why Legal AI Is Structurally Different

Most AI categories grow fast.

Few embed deeply.

Legal AI operates inside:

- Highly regulated environments

- High-liability workflows

- Document-heavy systems

- Jurisdiction-specific frameworks

- Client-confidential environments

Scaling here is harder than scaling consumer AI tools.

Trust must compound before revenue can.

From publicly shared review materials, Harvey reports:

- 92% monthly adoption rate

- 81% DAU/MAU growth since launch

- Over 213 million files analyzed

- Hundreds of product updates shipped annually

- Expansion to 250+ structured knowledge sources

- Integration with Microsoft 365 and enterprise document systems

Those signals suggest depth of usage — not surface experimentation.

Depth is what infrastructure companies build.

The Infrastructure Repricing

An $11B valuation on roughly $190M ARR implies a very aggressive revenue multiple.

But investors are not pricing current revenue alone.

They are pricing:

- Workflow embed potential

- Knowledge-layer lock-in

- Multi-practice expansion

- Enterprise contract durability

- Regulatory moat formation

If Legal AI becomes standard inside global firms, then the multiple makes strategic sense.

If it remains a powerful assistant layered on top of existing systems, valuation compression becomes likely.

This is the structural tension in vertical AI.

🟢 Bull Scenario: Legal AI Becomes Mandatory Infrastructure

In the optimistic case:

- Firms standardize on one or two dominant AI platforms

- Knowledge vaults increase switching costs

- Workflow builders deepen integration

- Global regulatory expansion strengthens moat

- ARR scales into the $500M–$1B range

At that point, Legal AI behaves like ERP for law firms.

Infrastructure companies tend to support premium valuation logic.

🔴 Bear Scenario: Legal AI Gets Bundled

The risk is not that Legal AI fails.

The risk is platform gravity.

Large incumbents — enterprise software providers, legal research platforms, and cloud hyperscalers — are expanding AI capabilities rapidly. History shows startup dynamics shift quickly once major platforms enter a category.

If AI drafting and review features become bundled into broader enterprise ecosystems:

- Pricing pressure intensifies

- Differentiation narrows

- Compute costs weigh on margins

- Retention becomes more competitive

Revenue may continue growing.

But multiples compress.

Infrastructure markets are powerful.

They are also unforgiving.

The Bigger AI & Emerging Tech Signal

Harvey’s valuation trajectory reveals something broader:

The next durable AI winners may not be horizontal platforms.

They may be vertical systems embedded in regulated industries.

Healthcare AI.

Financial AI.

Compliance AI.

Legal AI.

These markets are harder to enter.

But once trust compounds, they become sticky.

Venture capital appears to be shifting toward that thesis.

This shift reflects the broader structural reordering already visible across the 2026 startup cycle.

Why This Matters for Startups

For founders building in AI & Emerging Tech, the lesson is clear:

Model performance alone is not enough.

Durable value comes from:

- Data advantage

- Workflow ownership

- Compliance alignment

- Integration depth

- Switching costs

Harvey’s rise suggests that when vertical AI achieves institutional trust, capital responds aggressively.

But capital acceleration also raises expectations.

The jump from $1.5B to $11B valuation sets a high bar for execution.

Final Take

Legal AI is emerging fast.

But speed is not what justifies $11 billion.

Embedded workflow power does.

If Harvey continues converting usage into institutional dependency, Legal AI could become one of the first true AI infrastructure categories in professional services.

If competitive pressure narrows its differentiation, the valuation story changes quickly.

AI markets are maturing faster than previous technology cycles.

Legal AI may now be entering its infrastructure phase.

And infrastructure races rarely leave room for many winners.

Research Credit: Metrics referenced from publicly shared Harvey materials and funding coverage, including analysis compiled by Niko Ludwig.

Editorial Note: This article reflects independent analysis of publicly available information and broader AI ecosystem trends.