Inside the mega-deals, infrastructure bets, and policy shifts redefining venture capital’s relationship with deep technology.

Global venture capital entered 2026 with an unusual signal: capital is concentrating faster than innovation cycles themselves.

In February alone, global venture funding reached $189 billion, the largest monthly total ever recorded. Artificial intelligence startups captured roughly $171 billion of that capital, representing nearly 90% of all venture investment during the month.

But the headline number hides a more important structural pattern.

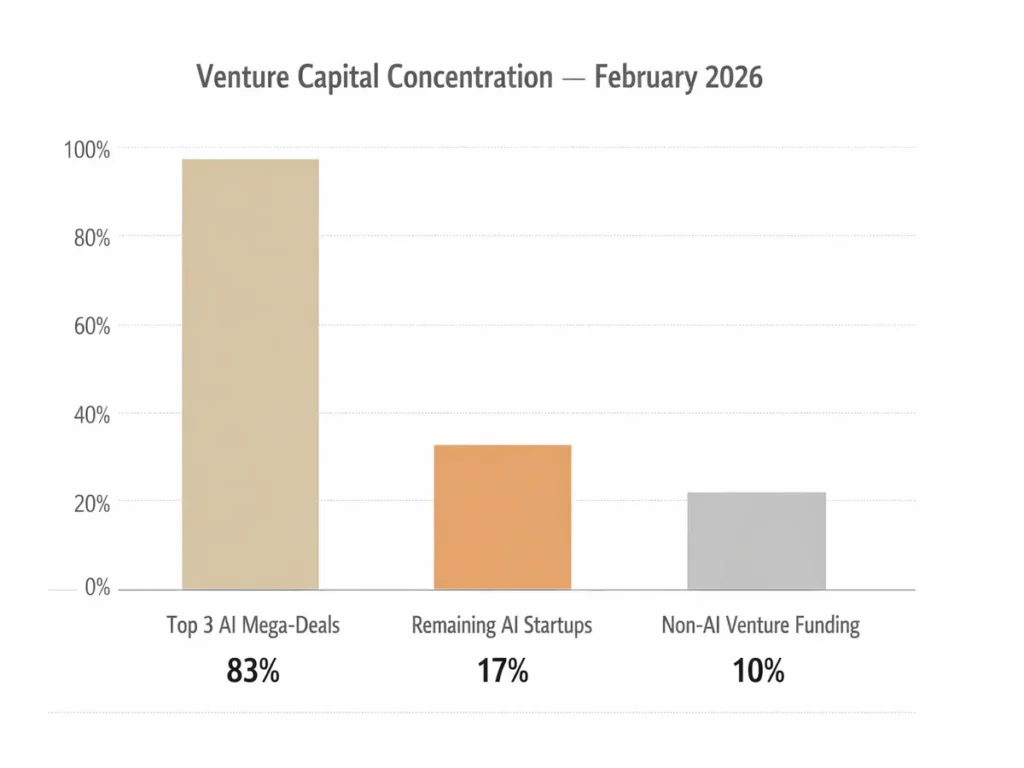

Most of that capital did not spread across hundreds of startups. Instead, 83% of February’s AI funding flowed into just three mega-deals.

The result is a venture market increasingly defined by capital concentration around infrastructure-scale companies, rather than the broad experimentation that characterized earlier AI cycles.

The Three Mega-Deals Driving the AI Capital Surge

The largest funding events of early 2026 reveal where investors believe long-term AI value will accumulate.

OpenAI: The $110 Billion Round

OpenAI closed the largest private funding round in technology history, raising approximately $110 billion at a valuation approaching $730 billion.

The round included participation from:

- Nvidia

- SoftBank

- Amazon

- sovereign wealth funds

- private equity investors

Rather than funding product expansion alone, the capital is expected to finance:

- hyperscale data centers

- GPU procurement

- global enterprise deployments

- development of next-generation frontier models

The scale of the investment reflects a growing consensus that AI model development is becoming infrastructure-level spending, similar to cloud computing during the 2010s.

Anthropic: $30 Billion to Compete in Frontier AI

Anthropic followed with a $30 billion Series G, valuing the company at roughly $380 billion.

Backed by strategic investors including Amazon and Google, the round positions Anthropic as the primary independent rival to OpenAI in frontier model development.

Unlike earlier AI funding cycles focused on experimentation, this round signals a shift toward enterprise-grade AI deployment and regulated-industry adoption.

Anthropic’s Claude models have been gaining traction in:

- financial services

- healthcare

- enterprise automation

The company’s strategy centers on agentic AI systems and safety-aligned models, two areas increasingly prioritized by large corporate buyers.

Waymo: Embodied AI Enters the Infrastructure Race

Alphabet’s autonomous vehicle subsidiary Waymo raised $16 billion at a valuation of roughly $126 billion.

Unlike the model-centric investments dominating AI headlines, Waymo’s funding reflects growing investor interest in embodied AI systems—physical infrastructure powered by machine intelligence.

Capital from the round will support:

- expansion of autonomous ride-hailing fleets

- simulation infrastructure

- robotics research and sensor systems

As AI moves from software into physical systems, sectors like robotics and autonomous mobility are beginning to attract infrastructure-scale investment.

A Venture Market Defined by Concentration

The scale of these deals reveals a growing divergence within venture capital.

The top three AI funding rounds in early 2026 account for an extraordinary share of global venture investment.

This dynamic has produced what investors increasingly describe as a “two-tier venture market.”

At the top tier:

- frontier AI labs

- compute infrastructure companies

- AI hardware firms

continue to raise massive capital rounds.

At the lower tier:

- early-stage startups

- research-heavy deep tech ventures

face more cautious funding environments.

The shift reflects a broader transition within venture capital itself: investors are moving away from speculative experimentation toward large, concentrated bets on companies capable of dominating infrastructure layers — a pattern increasingly visible across the emerging AI infrastructure investment cycle shaping the technology economy.

Visualizing the Capital Concentration

The scale of capital flowing into a small number of AI companies becomes clearer when viewed across the broader venture ecosystem.

AI Venture Capital Concentration — February 2026

| Category | Funding Share | Description |

|---|---|---|

| Top 3 AI Mega-Deals | 83% of AI funding | Frontier AI and autonomy companies capturing the majority of venture capital |

| Remaining AI Startups | ~17% | Hundreds of startups competing for the remaining AI funding |

| Non-AI Venture Funding | ~10% | All other venture categories combined |

This distribution reveals how dramatically venture capital has shifted toward infrastructure-scale AI bets.

Rather than diversified portfolios across thousands of startups, capital is increasingly concentrating around companies capable of building:

- global AI compute infrastructure

- frontier models

- autonomous systems

- enterprise AI platforms

In effect, venture capital is beginning to resemble infrastructure financing rather than traditional startup investing.

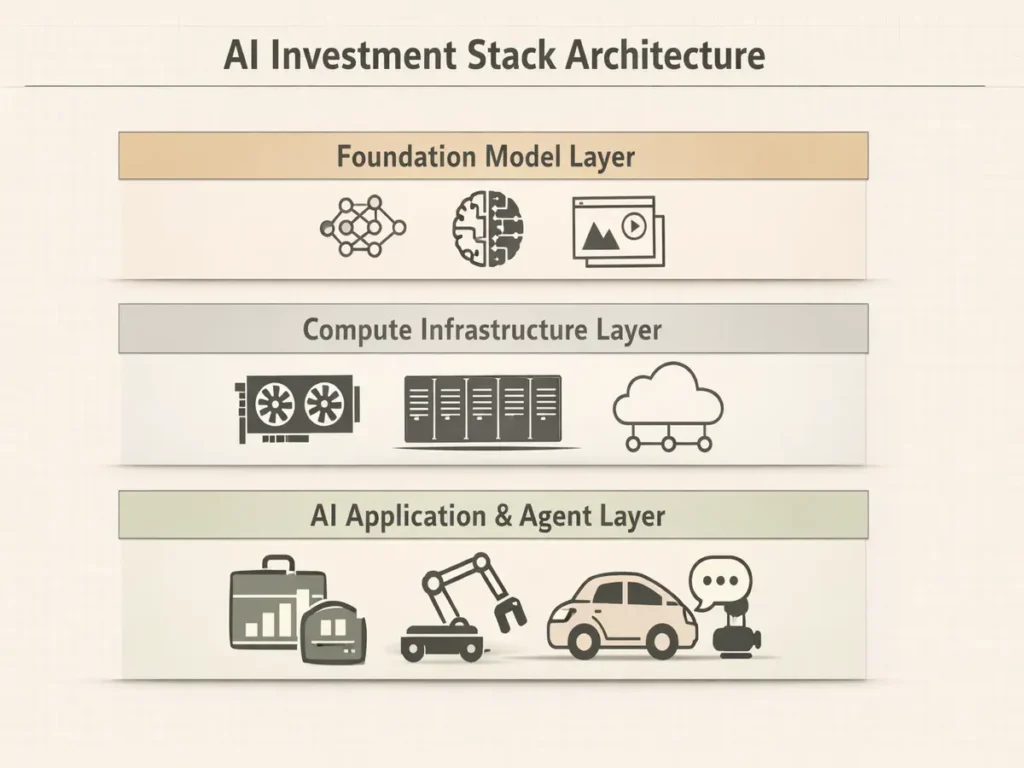

Where the Capital Is Actually Going

Beyond individual mega-rounds, the new AI investment cycle is reshaping how venture capital maps onto the technology stack itself.

The current AI capital wave is increasingly distributed across three structural layers:

Model Layer

Companies building frontier models and training infrastructure.

Examples include OpenAI, Anthropic, and emerging multimodal research labs.

Compute Layer

Infrastructure providers building the physical capacity required to train and deploy large models.

This includes:

- hyperscale data centers

- GPU clusters

- AI inference networks

Application and Agent Layer

Startups building enterprise AI systems that integrate models into real-world workflows.

This layer includes:

- enterprise AI platforms

- developer tooling

- agent orchestration software

Increasingly, these layers are connected through emerging context orchestration infrastructure that coordinates models, enterprise data, and intelligent agents.

Understanding how capital distributes across these layers helps explain why a small number of companies are absorbing an outsized share of venture funding.

Deep Tech’s Expanding Share of Venture Capital

Despite the concentration of capital, deep technology sectors continue to gain importance within the global venture ecosystem.

Over the past decade, deep tech’s share of venture funding has expanded from roughly 10% to nearly 24%.

In Europe, the shift is even more pronounced. Deep tech now accounts for 36% of venture investment across the region, driven by strong activity in:

- semiconductors

- robotics

- climate technology

- advanced materials

The expansion reflects growing investor confidence that deep technology platforms can generate long-duration competitive advantages, particularly when they intersect with AI.

Governments Are Now Co-Investors in Deep Tech

The capital intensity of deep tech development is also pulling governments deeper into venture ecosystems.

India announced a $1.1 billion deep tech fund-of-funds designed to support AI and advanced manufacturing startups through private venture capital partnerships.

Meanwhile, the European Innovation Council launched a €300 million STEP Scale-Up program targeting large deep-tech funding rounds.

These initiatives highlight an emerging geopolitical dimension of venture capital.

Technologies such as:

- AI

- semiconductors

- robotics

- quantum computing

are increasingly viewed not only as commercial opportunities but also as strategic national capabilities.

Early-Stage Deep Tech Still Struggles to Scale

Despite the enormous capital flowing into top AI companies, early-stage deep tech startups continue to face structural funding challenges.

Research-heavy ventures often require:

- longer development cycles

- significant hardware investment

- regulatory approvals

before generating revenue.

This has pushed many venture investors to prioritize companies with clearer commercialization pathways.

The result is a growing preference for AI-enabled applications built on top of deep technology infrastructure, rather than pure research ventures.

Defense Tech and Sovereign AI Are Emerging Themes

Another notable trend shaping deep tech investment is the rapid rise of defense technology.

Defense-related startups generated nearly $50 billion in deal value during 2025, with momentum continuing into early 2026.

Venture capital firms increasingly view defense technology as an attractive category because it combines:

- strong government demand

- long-term procurement cycles

- national security priorities

Sovereign AI infrastructure is emerging as a related theme.

Governments and investors alike are seeking domestic alternatives to dominant AI platforms — accelerating investment in national AI stacks and independent infrastructure layers.

The Infrastructure Phase of AI Venture Capital

Taken together, the funding data from early 2026 suggests a broader structural transition.

The first phase of the AI boom focused on experimentation and consumer applications.

The second phase now underway is centered on infrastructure scale, increasingly visible across the global enterprise AI infrastructure race.

This includes:

- foundation model development

- AI compute infrastructure

- autonomous systems

- robotics

- enterprise AI platforms

These sectors require dramatically larger capital commitments than earlier software startups.

But they also offer the potential to define the core infrastructure of the next technological era.

The Contrarian Question: What If AI Capital Overshoots Demand?

The extraordinary scale of capital flowing into AI infrastructure also introduces a structural risk.

Large technology companies are projected to spend more than $650 billion on AI infrastructure between 2025 and 2027.

Infrastructure cycles historically follow a familiar pattern.

Periods of rapid capacity expansion are often followed by temporary overcapacity, particularly when demand evolves more slowly than expected.

Similar cycles occurred during:

- the telecom infrastructure boom

- the early cloud computing expansion

If AI adoption grows more gradually than projected, the industry could briefly face excess compute capacity and compressed returns on capital investments.

That possibility does not invalidate the long-term AI infrastructure thesis.

But it introduces a critical dynamic for investors:

The companies that ultimately win the AI infrastructure race may not be the ones that raise the most capital first.

They may be the ones that deploy it most efficiently.

What Comes Next in the AI Venture Cycle

If the current trajectory continues, the next wave of venture investment may shift toward three emerging sectors:

- AI inference infrastructure powering real-time applications

- agent orchestration platforms coordinating autonomous systems

- physical AI platforms combining robotics, sensors, and AI software

These sectors represent the operational layer where AI moves from research breakthroughs into real-world economic infrastructure.

Editorial Takeaway

The record-breaking funding surge in early 2026 signals a transformation in how venture capital approaches deep technology.

Rather than spreading investment across thousands of startups, investors are increasingly concentrating capital around companies building the foundational layers of the AI economy.

Artificial intelligence is no longer treated as a speculative technology sector.

It is being financed as global infrastructure.

And infrastructure markets rarely produce many winners.

Research Context

This article synthesizes venture funding data from Crunchbase, TechCrunch reporting, European venture analyses, and industry investment research covering the period between February 1 and March 7, 2026.

Editorial Note

This article reflects independent TechFront360 analysis of venture capital flows shaping the global deep technology ecosystem and the increasing concentration of funding around AI infrastructure platforms.