Grand isn’t just building a payments startup. It is rebuilding how trust flows through global trade.

Grand, a Dublin-based AI payments startup founded by the team behind WhenThen, has raised $5 million in a pre-seed round led by 20VC — signaling a structural shift in how financial infrastructure is being rebuilt around real-time trust rather than static credit systems. With participation from NAP and Firedrop, the round reflects a deeper thesis that extends beyond payments: that the real bottleneck in B2B commerce is not access to capital, but the inability to continuously evaluate counterparties in real time as conditions change.

This is not a payments interface problem. It is a trust infrastructure problem.

The Problem: Credit Systems Built for a Slower Economy

For decades, B2B payments and trade finance have relied on static credit models built around periodic financial statements, delayed reporting cycles, and backward-looking risk scores, all of which were designed for slower, more predictable supply chains where change occurred gradually rather than continuously.

That model no longer holds.

Businesses today are forced to make high-stakes decisions — who to extend credit to, who to onboard, and how much exposure to take — using information that is often outdated by weeks or even months, which leads not only to mispriced risk but also to missed opportunities across entire trade networks.

Companies move slower. They under-extend credit. They avoid relationships they cannot confidently evaluate.

The friction is systemic.

The Founder Insight: Trust Is the Missing Layer

Grand’s founding team — Kirk Donohoe, Dave Brown, and Eamon Doyle — are not new to payments infrastructure, having previously built WhenThen and successfully exited to MangoPay, which gives them direct experience with the limitations of existing financial systems and how those systems behave under real-world constraints.

Their core insight is simple but structurally significant:

👉 Businesses don’t need better credit scores. They need continuous trust signals.

Instead of evaluating companies as static entities based on historical reporting, Grand aims to understand them as dynamic systems that evolve over time, where behavior is continuously observed and interpreted rather than periodically summarized.

That changes everything.

The Product: From Credit Snapshots to Continuous Intelligence

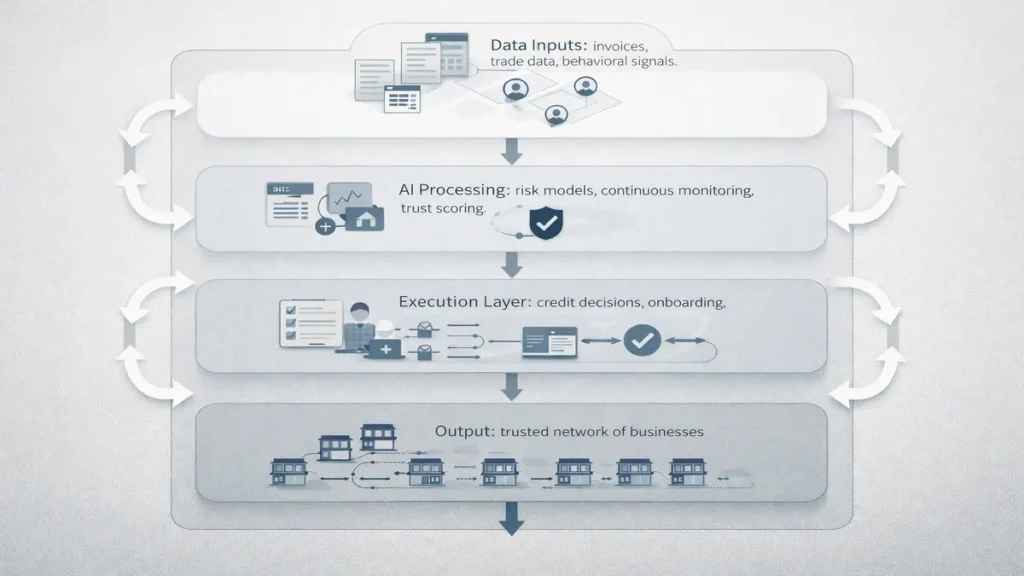

Grand’s first product, Grand Profile, is designed to reflect this shift by moving away from static credit assessments and toward continuous intelligence systems that capture how businesses actually behave in real operational contexts.

Rather than providing a fixed score, the system builds:

- continuous behavioral profiles

- real-time risk signals

- forward-looking reliability indicators

- evolving trust assessments

This fundamentally changes decision-making.

Not based on what a company reported last quarter. But based on how it behaves right now.

From hindsight to foresight.

The Bigger Bet: A Trust-Native Payment Network

The product itself is only the starting point, acting as an entry layer into a much larger system that Grand is attempting to build over time — a trust-native payment and credit network where financial interactions are governed by continuously updated intelligence rather than static evaluation frameworks.

In this model:

- businesses extend credit based on real-time trust

- payments flow within verified ecosystems

- counterparties are continuously monitored

- risk is dynamically priced

This represents a structural departure from traditional payment rails, which are fundamentally transaction-first systems.

Grand is building something different.

Trust-first.

Why This Matters: Payments Are Becoming Intelligence Systems

The payments stack is undergoing a quiet but important transformation, shifting from a system focused purely on the movement of money toward one that increasingly embeds intelligence directly into financial flows and decision-making processes.

Historically, payments and credit operated as separate layers, with transactions occurring independently of risk evaluation systems.

That separation is collapsing.

Because in B2B environments, money does not move without trust, and trust is no longer something that can be approximated through static scoring models — a shift increasingly visible in how AI is rebuilding financial execution layers, as seen in Accounts Receivable Is Breaking — Cleavr’s AI Is Rebuilding It as Infrastructure.

Grand sits directly at this intersection:

👉 payments + data + AI + risk intelligence

This is not a feature upgrade. It is a category shift.

The Market Pattern: AI Is Moving Into Financial Decision Layers

Grand is part of a broader transition across enterprise AI, where the most valuable systems are no longer those that simply visualize data or assist workflows, but those that directly influence financial outcomes by shaping how decisions are made at the operational level.

These systems increasingly operate across:

- pricing

- credit decisions

- revenue flows

- capital allocation

In this context, Grand is not just a payments startup.

It is an AI-driven financial decision layer embedded inside the infrastructure of trade — a pattern that aligns with the broader capital shift explored in AI Funding Is Splitting Into Infrastructure and Physical Intelligence Bets.

The Founder Advantage: Infrastructure Experience Compounds

One of Grand’s strongest advantages lies in the depth of its founding team, which has spent years working together across payment systems and infrastructure environments, building products that required integration across complex financial ecosystems.

Their experience at Mastercard Labs and their journey with WhenThen give them a strong foundation in:

- payment orchestration

- system integration

- regulatory navigation

- enterprise adoption cycles

This matters.

Because infrastructure companies are not built on ideas alone. They are built on execution depth and system understanding, both of which compound over time.

The Constraint Layer

The opportunity is clear. The constraints are equally structural.

Trust data is fragmented and difficult to standardize across industries, B2B adoption cycles are inherently slow and relationship-driven, incumbents such as banks and credit agencies remain deeply entrenched, and the accuracy requirements for any trust-based system are extremely high.

Most critically:

👉 trust systems only work if they are widely adopted

This creates a classic network effect challenge, where value increases with participation but initial adoption is difficult to achieve.

Why This Raise Matters

At $5 million, this is not a large round in absolute terms, but it is strategically important because it signals early investor conviction in a category that is still forming and not yet fully recognized as a standalone layer within financial infrastructure.

It reflects belief in:

- trust as infrastructure

- AI-driven financial decision-making

- payments evolving beyond transactions

20VC’s involvement reinforces this positioning.

This is not a bet on a feature. It is a bet on a new layer of the financial stack.

The Structural Shift: From Payments to Trust Infrastructure

Grand reflects a broader transition taking place across financial systems, where the traditional separation between payments, credit, and risk is being replaced by integrated systems that combine these functions into a single intelligence layer.

Old model:

- payments → transactions

- credit → static scoring

New model:

- payments → embedded intelligence

- credit → continuous evaluation

- trust → programmable layer

This is where the stack is moving — a transition similar to how control layers are emerging across AI systems, as outlined in Dash0 Hits $1B — Why AI Observability Is Becoming a Control Layer.

What Grand Is Actually Building

Grand is not simply building a payments company. It is attempting to construct a real-time trust layer for B2B commerce, where intelligence replaces static data, behavior replaces reporting, and trust becomes the foundation upon which financial interactions are executed.

In this system:

- intelligence replaces static data

- behavior replaces reporting

- trust replaces friction

And payments become a function of that system — reinforcing a broader shift toward deeper infrastructure layers similar to Spade Raises $40M to Own the Data Layer That Financial AI Cannot Function Without.

Editorial Close

Most startups in payments focus on improving speed, reducing cost, or refining user experience, but Grand is targeting a deeper problem that sits underneath all of those layers: how businesses decide who to trust in environments where information is incomplete and constantly changing.

Because in global trade, that decision determines everything.

Who gets paid. Who gets credit. Who grows.

And increasingly, how entire supply chains function.

Research Context

Based on company disclosures, Business Post reporting, funding data, and analysis of emerging AI-driven financial infrastructure and trust-based payment systems.

Editorial Note

This article reflects independent analysis of publicly available information and broader structural shifts in enterprise AI and financial systems.