While Silicon Valley scales general AI, Europe is hardening its own stack.

Europe is not trying to outrun Silicon Valley.

It is trying to insulate itself from it.

Mistral AI began as a benchmark challenger. Today it is building something heavier. A vertically integrated AI infrastructure layer rooted inside European regulatory and physical boundaries.

The benchmark race makes headlines. Infrastructure quietly compounds.

That distinction may determine which AI companies endure.

The Compute Pivot

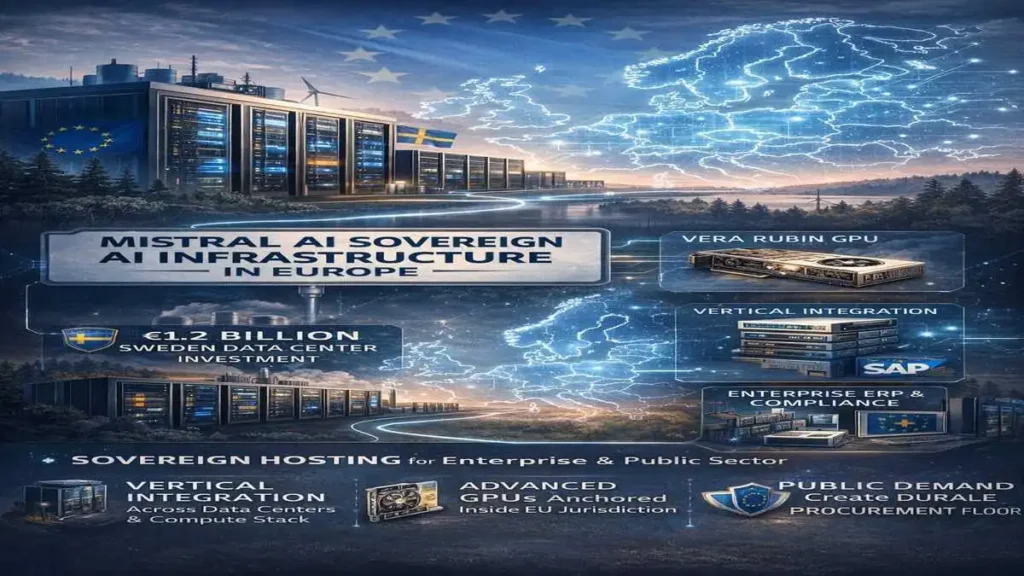

In February 2026, Mistral announced a €1.2 billion investment in a large-scale AI data center in Sweden, in partnership with EcoDataCenter. According to Reuters reporting, the project is designed to reduce dependence on U.S. hyperscalers.

This is not a model release.

It is a compute containment strategy.

Advanced NVIDIA hardware, including early deployment of next-generation GPUs, is being anchored inside European jurisdiction. Model development remains internal. Its interface layer, Le Chat, completes the operational loop.

Few startups attempt vertical integration at this stage.

Fewer attempt it in a capital-intensive domain dominated by trillion-dollar infrastructure firms. Once platform power consolidates at infrastructure scale, competitive dynamics change quickly.

Capital Is Choosing Containment

Europe accounted for roughly 20 to 25 percent of global AI venture allocation in 2025, according to aggregated PitchBook and CB Insights estimates — a dispersion that reflects the broader structural reset shaping the current AI capital cycle. North America still absorbs the majority of frontier model capital, but European flows are clustering differently.

They are favoring compliance-oriented infrastructure.

Public sector technology procurement across EU member states exceeds €150 billion annually. Even if a single-digit percentage shifts toward sovereign AI infrastructure, the revenue floor for regional providers becomes durable.

This is the quiet arithmetic behind Mistral’s strategy.

Governments do not optimize for viral adoption curves.

They optimize for jurisdictional control.

The Harder Financial Cluster

Global AI investment now exceeds $50 billion annually. Yet compare scale asymmetry:

• Anthropic’s latest round valued the company at approximately $380 billion

• Hyperscaler AI capex projections for 2026 exceed $650 billion collectively

• Europe’s total annual AI funding remains a fraction of U.S. frontier concentration

Mistral is not competing on financial scale.

It is competing on geographic anchoring.

If capital density determines frontier experimentation, jurisdiction determines long-term enterprise embedding.

That difference is structural.

From Model Shop to Sovereign ERP Layer

Strategic alliances with SAP and public institutions in France and Germany push Mistral further up the stack.

This is not about outperforming GPT-style general assistants.

It is about embedding AI into sovereign ERP systems used by public administrations and regulated enterprises.

Public agencies cannot risk sensitive data routing through foreign jurisdictions. That constraint, often framed as regulatory friction, becomes competitive leverage for a domestic provider.

The real battleground may not be developer APIs.

It may be procurement committees.

The Industrial Footprint

Infrastructure narratives often stay abstract.

The Swedish data center project changes that.

Compute capacity, energy sourcing, regional employment, and long-term hosting contracts create physical entrenchment. Power purchase agreements and cooling infrastructure do not pivot easily.

When AI becomes embedded in industrial-grade data centers tied to national energy grids, it stops behaving like venture software.

It behaves like utility infrastructure.

Utilities are valued differently.

Bull Case vs Structural Risk

Bull Case

If European governments and compliance-heavy enterprises prioritize domestic hosting, Mistral becomes the default sovereign AI layer. Long-term contracts expand. Switching costs rise. Revenue stabilizes under procurement cycles rather than consumer volatility.

Institutional embedding outlasts benchmark cycles.

Structural Risk

Vertical integration is expensive. Hyperscalers retain unmatched scale advantages. If U.S. providers offer compliant regional hosting at competitive pricing, Mistral’s differentiation compresses. Regulatory harmonization could erode geographic moat.

Sovereignty provides emotional clarity.

Infrastructure requires financial durability.

The valuation outcome depends on which prevails.

Europe’s Different Time Horizon

Silicon Valley optimizes for scale velocity.

Europe optimizes for contractual endurance.

These philosophies produce different capital structures and growth expectations. North American AI firms pursue API ubiquity. European AI firms pursue institutional embedding.

One maximizes developer ecosystems.

The other maximizes policy alignment.

Both can succeed.

They do not compound at the same speed.

The Quiet Ecosystem Tension

Fragmentation benefits regional providers.

It also increases systemic friction.

Global enterprises operating across jurisdictions must reconcile multiple AI stacks. Hyperscalers resist fragmentation because interoperability preserves scale economics. Sovereign containment introduces integration cost.

Europe’s bet is that regulatory gravity outweighs integration friction.

That assumption will be tested.

The Uncomfortable Reality

Europe is unlikely to dominate frontier benchmark headlines.

It may not need to.

If compliance-driven infrastructure becomes the default for public institutions and regulated sectors, revenue durability could outweigh model spectacle.

This is not about surpassing GPT benchmarks.

It is about surviving procurement cycles that outlast hype cycles.

Procurement cycles can stretch across decades.

Venture cycles rarely do.

Long-Term Implications

AI capital is no longer converging toward a single architecture.

The United States concentrates on orchestration layers and reasoning engines. China integrates AI into civic and industrial systems. India leans into workflow automation. Japan fuses AI with robotics. Europe builds containment.

Fragmentation reduces direct benchmark competition. The same infrastructure logic is visible in robotics capital allocation, where physical deployment and compute sovereignty increasingly intersect.

It increases infrastructural differentiation.

In five years, AI leadership may not be defined by model size. It may be defined by institutional depth and geographic entrenchment.

Mistral’s strategy signals Europe understands this calculus.

Final Take

Mistral AI is no longer just a model startup.

It is an infrastructure experiment inside regulatory boundaries.

If sovereignty becomes structural moat, Mistral stands to benefit disproportionately. If hyperscalers neutralize geographic differentiation, margin compression follows.

Either way, this is not a conventional scaling story.

It is a sovereignty calculation expressed through compute architecture.

And sovereignty rarely behaves like venture momentum.

Research Context: Funding figures and infrastructure announcements referenced from Reuters reporting, CB Insights and PitchBook AI investment ranges, and publicly disclosed company releases.

Editorial Note: This article reflects independent analysis of publicly reported information and broader AI ecosystem capital dynamics.