Inside the cohort redefining AI startup economics

AI startups are scaling faster than any technology companies in history. Funding rounds are larger, product cycles are shorter, and valuations compress years of growth into months.

Yet something deeper is shifting beneath the surface.

What appears to be a startup boom may instead mark the early formation of the next technology infrastructure layer. Frontier AI companies are institutionalizing earlier than previous cycles, as valuation, recurring revenue visibility, and enterprise embedment converge into a single growth phase that prioritizes durability over experimentation.

A small group of companies — Anthropic, Mistral AI, Perplexity AI, Harvey, Apptronik, and ElevenLabs — increasingly behave less like startups chasing traction and more like institutions securing long-term positioning.

The shift is subtle. Structurally, it is enormous.

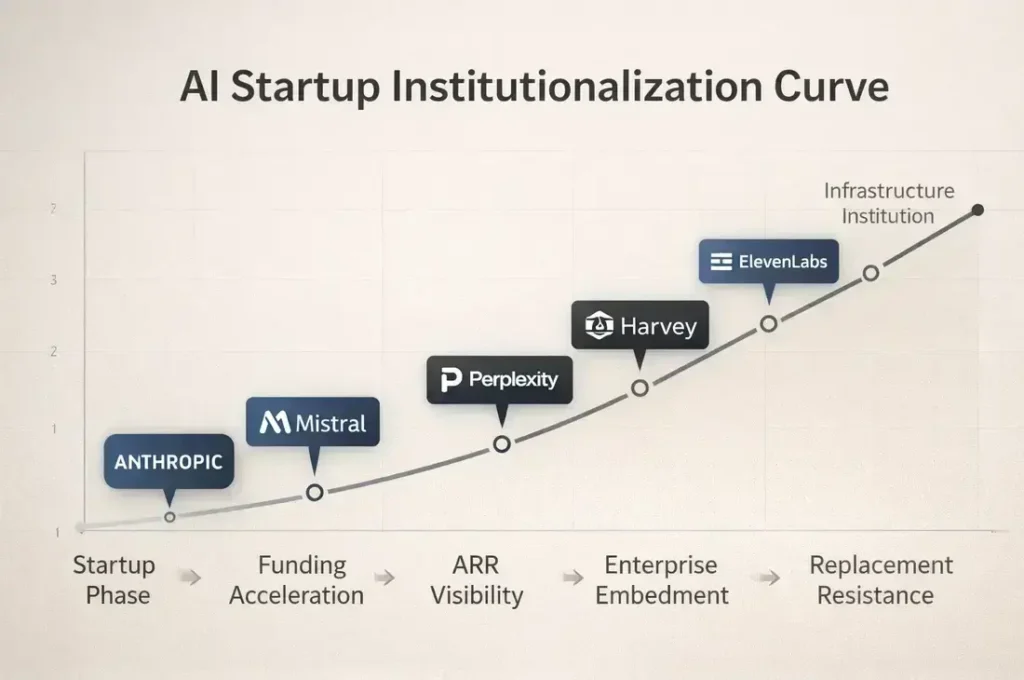

The Startup Disappearance Phase

Traditional startup narratives follow a predictable arc: build product, find distribution, raise capital, scale.

Frontier AI companies compress that sequence into one phase. They launch with infrastructure dependencies, enterprise customers, regulatory exposure, and multi-year compute commitments already in place, meaning growth is embedded rather than exploratory.

In this environment, the startup identity erodes earlier than expected. These companies are not simply scaling. They are stabilizing.

The Valuation Signals

Valuation trajectories reveal the shift more clearly than product announcements.

| Company | Approx. Valuation | Revenue Signals |

|---|---|---|

| Anthropic | ~$30B+ | Enterprise contracts, Claude monetization |

| Mistral AI | ~$6B+ | Sovereign deployments, enterprise licensing |

| Perplexity AI | ~$1B+ | Subscription growth, search distribution |

| Harvey | ~$11B | Enterprise legal ARR concentration |

| Apptronik | ~$935M+ funding | Robotics partnerships, industrial pilots |

| ElevenLabs | ~$11B | High ARR per employee, voice infrastructure adoption |

The pattern is consistent. Capital is pricing long-term embedment rather than short-term growth, increasingly resembling infrastructure underwriting.

The Funding Cycle Compression

Frontier AI startups are not only raising more capital. They are raising faster, in larger increments, and with shorter intervals between rounds.

The institutionalization timeline that once took a decade is now unfolding within a single funding cycle.

Funding Cycle Snapshot (2023–2026)

Anthropic — multi-billion hyperscaler rounds → enterprise infrastructure formation

Mistral — seed to unicorn speed → sovereign AI urgency

Perplexity — distribution-driven funding → interface positioning

Harvey — enterprise scaling rounds → vertical infrastructure pricing

Apptronik — robotics expansion → physical AI timelines

ElevenLabs — successive valuation jumps → multimodal leverage

Funding is increasingly positioning capital — securing ecosystem placement before markets stabilize. This dynamic mirrors the broader AI capital repricing cycle reshaping venture timelines.

Verified Company Context (Entity Layer)

Anthropic — Founded by former OpenAI researchers; hyperscaler partnerships tie model development to cloud infrastructure.

ARR signal: enterprise revenue trending contract-based.

Mistral AI — Fastest European AI unicorn trajectory driven by sovereign demand.

ARR signal: licensing revenue tied to regional deployments.

Perplexity — AI answer engine challenging search workflows.

ARR signal: subscription tiers introduce recurring consumer revenue inside search.

Harvey — Legal AI embedded inside major law firms.

ARR signal: concentrated enterprise ARR creates infrastructure durability.

Apptronik — Robotics platform moving from research into industrial pilots.

ARR signal: multi-year automation contracts rather than SaaS churn.

ElevenLabs — Voice infrastructure spanning creators, gaming, and enterprise localization.

ARR signal: unusually high ARR per employee indicates operating leverage.

Taken together, these signals describe architecture rather than competition. This shift reinforces how AI infrastructure is becoming the primary competitive layer.

The cohort spans multiple strategic geographies, with U.S. enterprise AI, European sovereign infrastructure, and industrial robotics converging into a shared institutional trajectory.

ARR, MRR, and the New Credibility Metric

Revenue composition reinforces the shift.

Enterprise AI firms increasingly prioritize predictable recurring revenue over rapid user expansion. Harvey’s concentration across law firms, ElevenLabs’ subscription expansion, and Perplexity’s paid tiers illustrate the move toward duration.

MRR stability now sits alongside growth as a credibility metric. Revenue duration is becoming the language investors use to interpret defensibility.

Across these companies, recurring revenue visibility is beginning to outweigh user growth velocity as the primary signal of maturity. This shift reframes AI startup progress from traction narratives toward institutional durability cycles.

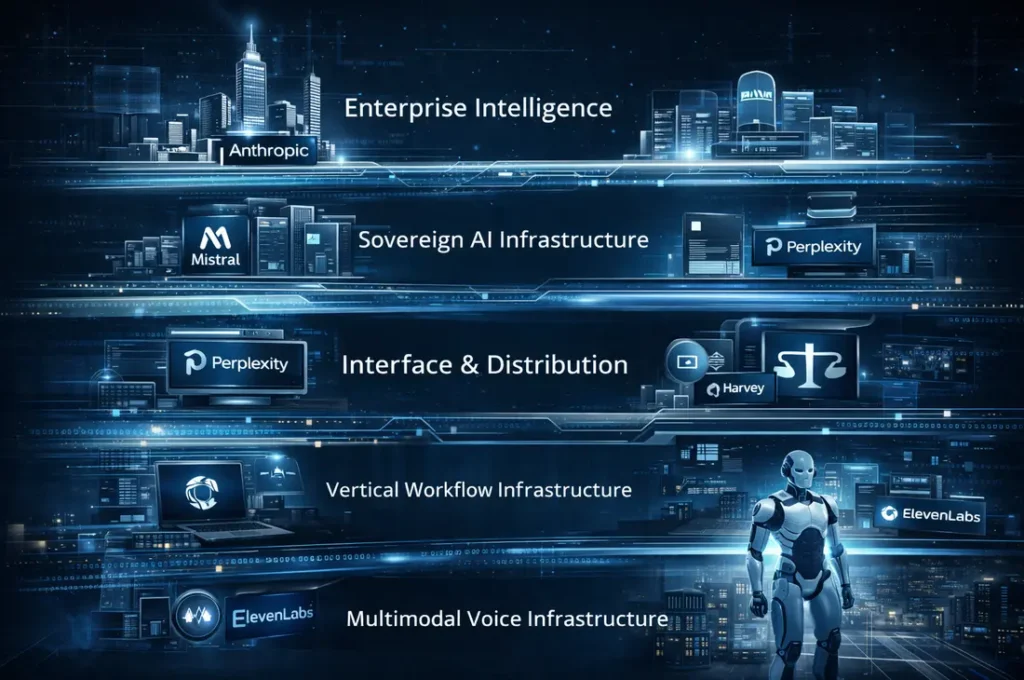

Stack Positioning: Different Layers, Same Outcome

- Anthropic — enterprise intelligence

- Mistral — sovereign infrastructure

- Perplexity — interface & distribution

- Harvey — vertical workflow infrastructure

- Apptronik — physical execution

- ElevenLabs — multimodal voice infrastructure

Competition is not horizontal. It is architectural. This architecture is unfolding within a fragmenting global AI landscape.

Why Each Startup Feels Older Than It Is

Anthropic behaves like a regulated vendor before public markets. Mistral operates like geopolitical infrastructure. Perplexity negotiates platform-style distribution economics. Harvey mirrors enterprise incumbents. Apptronik follows industrial robotics timelines. ElevenLabs demonstrates infrastructure-level leverage unusually early.

The startup label persists. The operating logic does not.

Founder Psychology Is Shifting

This structural transition is reshaping founder decision-making.

Instead of chasing traction, frontier AI founders increasingly design for replacement resistance. Governance, ecosystem positioning, and compute strategy shape roadmaps as much as product iteration.

Founder psychology is moving from acceleration toward permanence.

The Contrarian Insight: Distribution Is Becoming the Primary Moat

Capability gaps are compressing. Distribution, integration, and institutional trust are emerging as the dominant defensibility layer.

Perplexity partnerships. Harvey embedment. Anthropic governance positioning. ElevenLabs creator ecosystems.

Capability spreads horizontally. Embedment compounds vertically.

The moat is not intelligence. It is placement.

What This Means for Venture Capital

If frontier AI startups transition into infrastructure earlier, venture timelines change.

Execution risk replaces product risk. Duration risk replaces adoption risk. Capital allocation increasingly resembles infrastructure financing.

Strategic Implications for the Ecosystem

For founders, platform choice becomes structural dependency.

For investors, embedment potential outweighs feature velocity.

For incumbents, partnership timing determines positioning.

Infrastructure gravity reorganizes ecosystems around early anchors.

The Forward Signal: Replacement Resistance Becomes the Metric

The next decade may not be defined by which AI startup grows fastest, but by which one becomes hardest to replace.

Procurement cycles, compliance layers, workflow integration, and data gravity create switching friction that compounds over time.

The next funding cycle may reward replacement resistance more than growth velocity.

Progress is increasingly measured through replacement resistance.

The Moment When Startups Stop Being Startups

Every technology cycle contains a point when the most important companies quietly stop behaving like startups.

Frontier AI appears to be approaching that moment unusually early.

The defining question is no longer which startup grows fastest. It is which startup stops behaving like one first.

Frontier AI startups are entering a phase where valuation, recurring revenue, and institutional embedment converge — producing companies that institutionalize far earlier than previous cycles.

The companies shaping this phase are not simply growing faster. They are stabilizing earlier.

Research Context: This article synthesizes publicly reported funding data, ARR signals, enterprise deployment patterns, and ecosystem positioning across leading frontier AI startups.

Editorial Note: This analysis reflects independent interpretation of structural shifts shaping the global AI startup landscape.